{kind=link}

Having children is never easy, especially with the high cost of living in Singapore.

To cut costs, the government introduced the Baby Bonus Program, which gives cash rewards to encourage Singaporeans to have more children.

With the Baby Bonus, parents need a Child Development Account (CDA) in order to receive grants and cash rewards from the government.

How does the CDA work? Is there any way I can make the most of it?

Here is a quick guide on how to maximize your child’s CDA account and get the most out of your baby bonus rewards!

TL; DR: How to Maximize Your Child’s CDA Account

- Open your CDA with a bank with high interest rates

- Maximize the government’s dollar-for-dollar match

- Purchase an integrated sign plan approved by MediSave for your child

- Use your child’s CDA to pay for most of their expenses

Want to talk about parenting hacks to save you money? You can do this in the Seedly community!

What is the Child Development Account (CDA)?

The CDA is a special children’s savings account that can be opened with POSB / DBS, OCBC or UOB banks to build up the savings that can be spent on approved purposes.

The CDA account falls under the baby bonus program, which is part of the marriage and parenting package.

There is a Baby Bonus Cash Gift component and a Baby Bonus CDA component under this program.

What does my child get for opening a CDA account?

When you open a CDA account for your child, you get the following benefits:

1. First step Grant

You will receive $ 3,000 deposited into your child’s CDA under the government’s CDA First Step Grant.

2. Dollar-for-dollar comparison of savings

For those who didn’t know, the government will also match every dollar you save to your child’s CDA account.

That means if you deposit $ 3,000 into your child’s CDA account, the government will also deposit $ 3,000 in the same account!

However, there is a cap of $ 3,000 (1st child), $ 6,000 (2nd child), $ 9,000 (3rd, 4th child), and $ 15,000 (5th child and above) dollar-for-dollar matching -Scheme.

As announced in late February 2021, the dollar-for-dollar reconciliation for the second child was increased from $ 3,000 to $ 6,000.

So as long as your child is

1) a Singaporean and

2) whose Date of Birth or Estimated Delivery Date (EDD) is on or after January 1, 2021 is eligible for the higher settlement of $ 6,000.

Below is a quick rundown of how much money you can get from the government through the Baby Bonus Program:

| Baby bonus | Payout (1st child) | Payout (2nd child) | Payout (3rd, 4th child) | Payout (from 5th child) |

|---|---|---|---|---|

| Cash gift | $ 8,000 | $ 8,000 | $ 10,000 | $ 10,000 |

| First Step Grant (CDA) | $ 3,000 | $ 3,000 | $ 3,000 | $ 3,000 |

| Dollar-for-Dollar Matching (CDA) | $ 3,000 | $ 6,000 (extended from 2021) |

$ 9,000 | $ 15,000 |

| total | $ 14,000 | $ 17,000 | $ 22,000 | $ 28,000 |

How Can You Maximize Your Child’s CDA Account?

There are some banks where you can open a CDA account for your child.

It is wise to compare these different bank accounts so that you choose one that will yield the highest interest rates for your child.

Here we did a quick comparison of POSB, OCBC and UOB CDA accounts:

2. Maximize the government’s dollar-for-dollar game

As mentioned above, the government does a dollar-for-dollar reconciliation when you fund your child’s CDA account. Here is the maximum you can charge to maximize this benefit:

| Maximum amount you can deposit to receive dollar-for-dollar reconciliation | Government dollar-for-dollar matching | Total (excluding cash gift and first CDA step) | |

|---|---|---|---|

| 1 child | $ 3,000 | $ 3,000 | $ 6,000 |

| 2nd child | $ 6,000 | $ 6,000 | $ 12,000 |

| 3rd, 4th child | $ 9,000 | $ 9,000 | $ 18,000 |

| 5th child | $ 15,000 | $ 15,000 | $ 30,000 |

3. Purchase an integrated shield plan approved by Medisave for your child

An integrated shield plan is an addition to your MediShield life insurance plan. It offers additional benefits from private insurers that can help cover large hospital bills and select costly outpatient treatments.

It is beneficial if your child is insured at a young age as they will not be excluded from pre-existing conditions. With dollar-for-dollar matching, you essentially pay half the premiums!

So why not use MediSave to pay for an integrated sign plan?

Of course, your child will also get their MediSave account with $ 4,000 which is provided by the government.

While you can use your child’s MediSave payment for the integrated shield plan, it is much better to use their CDA account as you get a higher interest rate (5 percent) with your money in your MediSave account than with the CDA account (2 percent).

4. Use your child’s CDA to pay for most of their expenses

If you choose to maximize the dollar-to-dollar matching scheme, you will have $ 9,000 in your child’s CDA (assuming this is your first child).

Your child’s CDA can only be used in a list of approved expenses, some of which include:

- Payment for approved day care centers and kindergartens

- Medical expenses for your child

- Multivitamins, dietary supplements

- Optical care, glasses and contact lenses for the child.

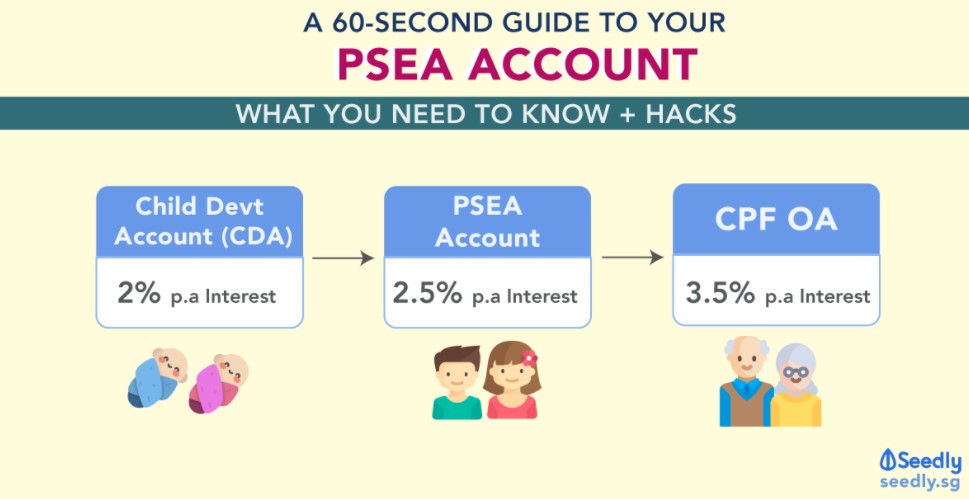

What happens to my child’s CDA account after they grow up?

When your child turns 13, the money not used from their CDA account will be automatically transferred to their post-secondary education account!

This account can be used for post-secondary school activities.

This article was first published in Seedly.